Hello Marathoners-

I hope everyone is doing well and surviving winter, wherever this note finds you. I was fortunate enough to escape both of the major Northeast snowstorms in January and February, during vacation time in Miami. But we’ll see what the next month brings.

With spring around the corner, it’s always a good reminder that seasons change—both in weather and in markets. This month, I wanted to share a few thoughts on risk, inflation, and why the biggest threats to long-term investors aren’t always the ones that dominate the headlines.

A while back, as I was taking on a new client who had been served rather poorly by a different firm, the client (a retiree) told me something that stuck with me.

“I’m not worried about the stock market anymore,” he said.

“I’m worried about running out of money.”

He had done almost everything right. For decades he saved diligently, avoided excessive debt, and invested carefully. By the time he retired he had built what most people would consider a very comfortable nest egg. But when we reviewed how his money was invested, something stood out. Nearly all of it had been moved into what he described as “safe investments.”

Cash.

Certificates of deposit.

Short-term bonds.

On the surface, the pre-existing strategy seemed perfectly sensible. His account balance barely moved. Market downturns didn’t bother him. The portfolio looked stable and predictable. But when we projected the next 20–30 years, a different risk began to appear. Not the risk of losing money in the market--the risk of slowly losing purchasing power.

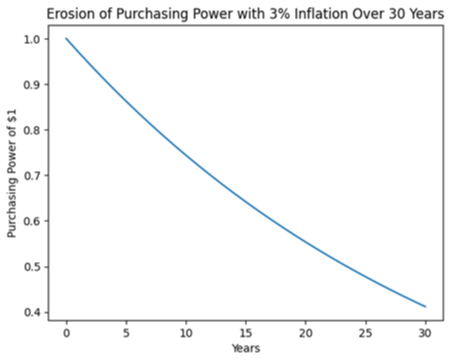

Inflation rarely feels dramatic in any given year, but over long periods it compounds quietly and relentlessly. Over the past century, inflation in the United States has averaged roughly 3% annually. At that rate, prices can rise more than two times over a typical 30-year retirement, meaning a dollar today could lose around 60% of its purchasing power over that period.

The chart below shows how that erosion works.

What starts as $1 of purchasing power can shrink to roughly 40 cents over three decades. Which raises a more important question than “What will markets do this year?”

The real question is: Will your portfolio keep up with the rising cost of living over decades?

The Illusion of Safety

Some investors try to eliminate risk by avoiding stocks entirely, and after volatility has already hit. Cash and bonds feel safe because their prices fluctuate less. But stability can sometimes be deceptive.

Thirty years ago:

- The Consumer Price Index stood at 156

- Today it stands around 326

Prices roughly doubled over that period.

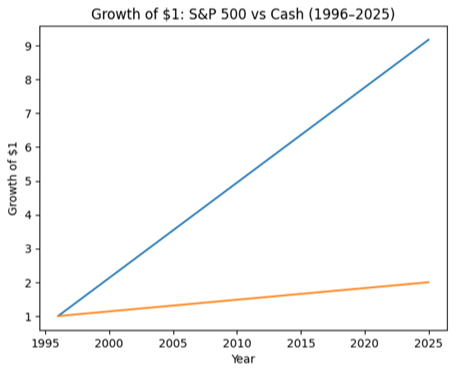

Meanwhile something interesting happened in the stock market.

The dividend income from companies in the S&P 500 increased from $14.89 in 1996 to $78.51 in 2025—more than a fivefold increase.

Even more striking, the S&P 500 index itself rose from roughly 741 to nearly 6,800 over that same period.

And that happened despite multiple recessions, wars, financial crises, and market crashes along the way.

The lesson is not that markets move smoothly—they clearly do not.

The lesson is that short-term volatility and long-term risk are not the same thing.

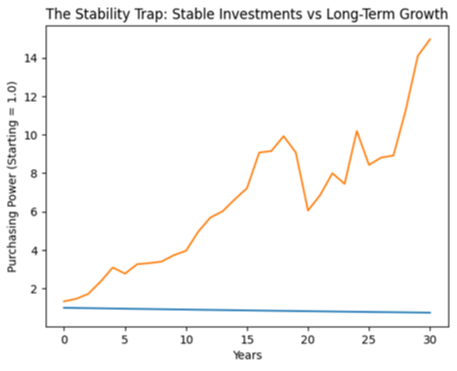

The Stability Trap

Below is a simple illustration of this idea. A portfolio invested in very stable assets may appear safe because its value barely fluctuates. But if the return does not keep up with inflation, its purchasing power gradually declines.

Meanwhile, a more volatile portfolio may experience ups and downs along the way—but historically has had a much better chance of growing purchasing power over time.

The Crisis Investors Are Always Waiting For

Another reason investors gravitate toward “safe” assets is fear that something catastrophic may happen to the financial system itself. One example that resurfaces regularly is concern about the U.S. national debt.

The numbers are certainly large, and eventually the trajectory of the debt must change, however investors should notice something interesting. Despite these concerns, global investors continue to lend money to the United States at relatively low interest rates.

For example, in 2016 the yield on the 10-year U.S. Treasury was just 1.85%, reflecting strong global confidence that the U.S. would repay its obligations. If investors truly believed a debt-driven collapse was imminent, those rates would likely look very different.

The Problem With Predicting Crises

History also teaches us something humbling. The risks that dominate headlines are often not the ones that cause the greatest damage.

Over the past two decades, investors have worried about:

- Y2K

- SARS

- The Eurozone collapse

- Government shutdowns

- Fiscal cliffs

- Pandemic scares

Each was widely discussed as a potential economic catastrophe. Yet markets ultimately navigated them all. Ironically, the crisis that did reshape the financial system in 2008 came from somewhere few people expected: the U.S. housing market. It was an unknown unknown.

The Real Goal of Investing

For long-term investors, the goal is not to predict every crisis--it’s to build a portfolio capable of growing and adapting over time.

Despite recessions, wars, pandemics, and political uncertainty, the global economy has historically continued to expand. Innovation increases productivity, businesses evolve, new industries emerge. And over long periods, markets have reflected that progress.

Successful investing has never been about predicting the next crisis.

It’s about ensuring that the money you save today can support the life you want tomorrow.

Retirement.

Financial independence.

Security for your family.

Because in the end, the greatest financial risk may not be market volatility.

It may simply be running out of purchasing power.

Important Financial/Tax Planning Issue To Cover: The “SALT Torpedo”

There is another financial planning issue that has quietly emerged in recent tax legislation. Planners sometimes refer to it as the “SALT torpedo.” The name sounds dramatic, but the concept is fairly simple.

“SALT” refers to State and Local Taxes—things like state income taxes and property taxes that can be deducted on your federal tax return. Recent tax changes temporarily increased the amount taxpayers can deduct from $10,000 to as much as $40,000.

That sounds like good news—and for many households it is. But there’s a catch. For households with income roughly between $500,000 and $600,000, that larger deduction begins to phase out quickly. As income rises through that range, taxpayers gradually lose the deduction. The result is that each additional dollar earned in that band can be taxed at a much higher effective rate than expected.

In some cases, earning an extra $100,000 can increase taxable income by more than that amount because deductions disappear at the same time. That sudden jump in taxes is what planners call the “SALT torpedo.”

Why This Matters

For many of our clients who are still in their peak earning years, this may be simply unavoidable, but if it’s any consolation, this higher cap is scheduled to sunset after 2029. Keep working and earn as much as you can, to get to that magical place of financial independence sooner!

But for those with household incomes in this territory (or could be soon if you’re considering a phased retirement/semi-retirement with gradual income reduction), definitely something we should pay close attention to. Especially in years when income temporarily spikes—for example:

- Exercising stock options

- Selling appreciated investments

- Receiving a large bonus

- Selling a business or property

- Doing a large Roth IRA conversion

When several of these events happen in the same year, they can push income into the phase-out zone and trigger the loss of deductions.

The good news is that in many cases, the impact can be reduced by:

- Spreading income like Inherited IRA distributions across multiple years, if possible

- Timing large transactions carefully

- Offsetting gains with losses

- Making tax-efficient charitable gifts

- Using retirement contributions to lower taxable income

Overall point: Taxes are one more reminder that financial planning isn’t just about investments. It’s also about coordination and timing. Large financial decisions—selling a property, exercising options, making Roth conversions, or realizing large gains—can have very different outcomes depending on when they occur.

Careful planning helps avoid surprises and ensures that more of your wealth continues working toward your long-term goals.

Thanks for taking the time to read this! If you have any questions about your portfolio or plan, please feel free to reach out. We always enjoy the opportunity to connect. Have a great weekend.

-Charlie

Chart sources: OpenAI/ChatGPT