Market Summary

Equity markets finished the week lower as investors continued to rotate out of mega-cap technology and AI-related names that have powered this year’s gains. Despite the headline weakness, performance beneath the surface was more balanced. Several defensive and value-oriented sectors advanced, and smaller companies held up relatively well, suggesting the market is undergoing a healthy rebalancing rather than a shift toward broad risk aversion.

Late in the week, expectations for a potential Federal Reserve rate cut strengthened meaningfully, helping drive a more constructive tone into Friday’s session.

The Economy

Economic data pointed to a continued moderation across key areas. Jobless claims remained stable, consumer sentiment held firm, and broader readings on hiring and activity reinforced the view of a cooling, but still resilient, economy. A continued temporary pause in several federal data releases added uncertainty but did not meaningfully alter the overall macro-outlook.

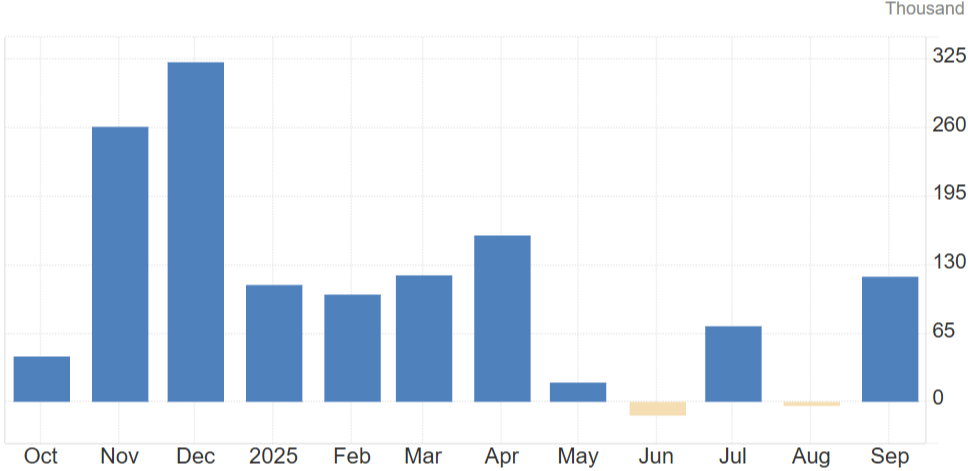

The September Jobs report was originally scheduled for release on October 3rd, but was delayed due to the longest Federal Government shutdown in U.S. history. The release of the October Employment Report has been cancelled.

The September report showed a rebound in job growth following recent weakness. It is the largest jump in five months and conducive to a slowing, yet resilient, labor market.

U.S. Non-Farm Payrolls - September 119K

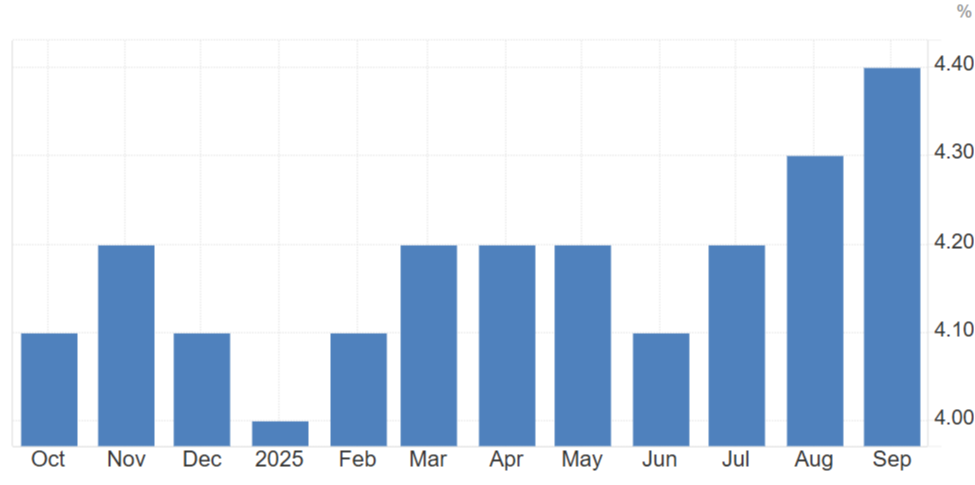

U.S. Unemployment - September 4.4%

The Fed

The Federal Reserve was a central focus as comments from New York Fed President John Williams suggested the door is open to cutting interest rates as early as December. Market expectations quickly adjusted, with the probability of a December rate cut rising from roughly 40% to nearly 75%. Treasury yields declined in response, providing support to rate-sensitive sectors and boosting small- and mid-cap stocks late in the week.

Geopolitics

Geopolitical developments were relatively muted and had limited direct impact on market performance. While ongoing global conflicts and trade considerations remain part of the broader backdrop, investors were more focused this week on domestic economic data and Federal Reserve policy signals.

Market-Specific

Selling pressure was concentrated within technology and semiconductor stocks, where investors took profits after a strong year of performance. Nvidia (NVDA) delivered another impressive earnings report, but its shares still retreated as elevated expectations and crowded positioning weighed on sentiment.

Other sectors, including health care, communication services, and consumer staples showed relative strength. Several companies in these sectors reached new 52-week highs, underscoring a shift toward more stable, less valuation-sensitive areas of the market.

Market breadth improved even as mega-cap stocks pulled back, reflecting an even more distribution of performance across sectors.

The rotation toward defensive and value-oriented stocks continued, helping balance volatility in technology. Small- and mid-cap indices outperformed large-cap peers, aided by falling yields and improving rate-cut expectations.

Overall, the recent weakness appears more reflective of positioning adjustments and recalibration of expectations than a deterioration in fundamentals. If improving breadth persists and policy expectations remain supportive, equities may regain steadier footing as we move toward the final month of the year.

The Week Ahead

This week, with Nvidia’s earnings release behind us and giving the market a point of relief, attention will turn towards the economy and rate expectations. Key economic data includes retail sales and the Fed’s preferred gauge for inflation as market participants look for signals towards the next rate decision. The market will be looking for additional confirmation that economic growth is slowing at a measured, orderly pace and supportive of rate-cut expectations.

Additionally, participants will be looking for the ability of technology and AI-related stocks to stabilize after recent weakness.

As always, please reach out with any questions and thank you for your Trust.

Respectfully,

Michael Neill, CFA

Chart Sources: TradingEconomics