Market Summary

Markets delivered a textbook example of post-Fed rotation last week. While a long-anticipated rate cut initially lifted risk sentiment, sharp reversals in AI and mega-cap tech ultimately pulled growth-heavy indices lower. Beneath the surface, however, strength in cyclicals, financials, and smaller-cap stocks reflected improving confidence in the economic outlook and a belief that gradually lower rates remain supportive. With policy now less restrictive but not aggressively accommodative, markets appear increasingly focused on earnings quality, economic durability, and breadth - rather than momentum alone.

The Economy

Economic data supported a ‘cooling but stable’ narrative. Labor market indicators remained resilient: job openings exceeded expectations, weekly claims stayed contained, and wage growth continued to decelerate—an encouraging signal for inflation. Manufacturing and leading indicators pointed to slower momentum, but not outright contraction risk. Housing and credit-sensitive areas responded positively to falling rates, reinforcing optimism around demand heading into year-end.

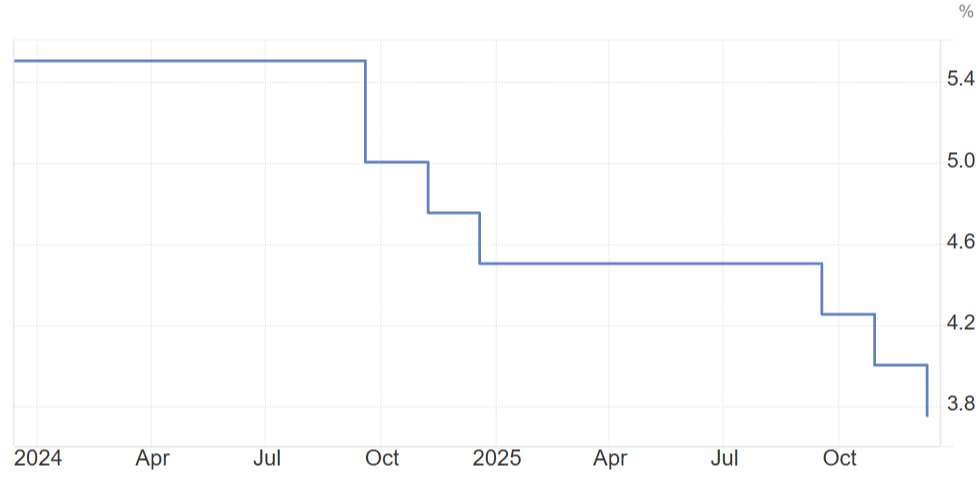

The Fed

The Fed delivered a 25-basis-point rate cut but paired it with deliberately cautious guidance – a classic “hawkish cut.” Fed Chair Powell emphasized a meeting-by-meeting approach, noting the policy rate now sits within a broad range of neutral estimates. Updated projections showed fewer cuts ahead but stronger GDP growth and lower inflation expectations, which markets ultimately interpreted as modestly dovish. The Fed also announced temporary Treasury bill purchases to stabilize reserves, adding liquidity without signaling aggressive easing. Bond yields initially fell but finished the week mixed as investors recalibrated expectations.

U.S. Fed Funds Interest Rate 3.50 - 3.75%

Geopolitics

Geopolitical risk played a secondary role but influenced sector-level moves. Semiconductor stocks reacted to renewed concerns around U.S. and China technology restrictions, contributing to volatility in chipmakers. Energy markets were shaped by OPEC+ maintaining output levels, while fertilizer and materials stocks responded to supply disruptions tied to Eastern Europe. Overall, geopolitical headlines amplified rotation rather than driving broad risk-off behavior.

Company Specific

Earnings reactions defined the week’s leadership shift. Several high-profile AI beneficiaries sold off despite solid results, reinforcing concerns that parts of the market remain priced for perfection. Disappointing revenue trends and cautious guidance from select tech names – particularly from Oracle (ORCL) – accelerated profit-taking across semiconductors and mega-cap growth. In contrast, industrials, banks, homebuilders, and materials stocks responded favorably to lower rates and improving economic projections. Notable strength also emerged in select consumer and healthcare names following earnings beats, guidance upgrades, and favorable regulatory developments.

Week Ahead

This week, economic data will likely be a primary driver with labor market and inflation data for November taking the spotlight. Retail sales will also be in focus as a headline gauge for consumer spending heading into year-end. Releases will also include some catch-up data labor, retail spending, and housing from October – stemming from the government shutdown. Earnings data will be relatively light outside a handful of names, including Micron Technologies (MU) on Wednesday.

As always, thank you for your trust and please reach out to us with any questions.

Respectfully,

Michael Neill, CFA

Chart sources: Tradingeconomics