Market Summary

The equity market fell short of its fourth consecutive weekly advance as stronger-than-expected economic data and Fed commentary helped shift interest rate expectations, offsetting AI-related enthusiasm.

Major indices found new highs early Monday spurred by the announcement of Nvidia’s partnership with OpenAI, which included an up to $100 billion investment from Nvidia in exchange for OpenAI deploying at least 10 gigawatts of Nvidia’s systems in the expansion of AI infrastructure – a massive project with the power usage demand comparable to what is needed to power all of New York City.

Sentiment quickly reversed as doubts for the ambitious project coincided with the announcement of five new AI data center sites from the equally ambitious Stargate Project, which failed to reignite any momentum. Investors also had a muted reaction to earnings from data storage and memory chip leader, Micron (MU), on Wednesday.

It is likely that recent commentary by Fed Chair Powell, citing that the market appears ‘fairly highly valued’ has contributed to some valuation concerns, prompting a slight slowdown in AI-driven momentum.

Economic data this week pointed towards resilient – even strong – consumer spending along with a still resilient labor market and stable (yet elevated) inflation. These considerations, along with commentary from several Fed members, somewhat dampened expectations for further rate cuts before year-end and contributed to some choppiness in the equity market.

At the same time, evidence of strong consumer spending and higher-than-expected GDP growth for the second quarter helped bolster growth optimism and rallied the market late in the week on Friday, paring weekly losses.

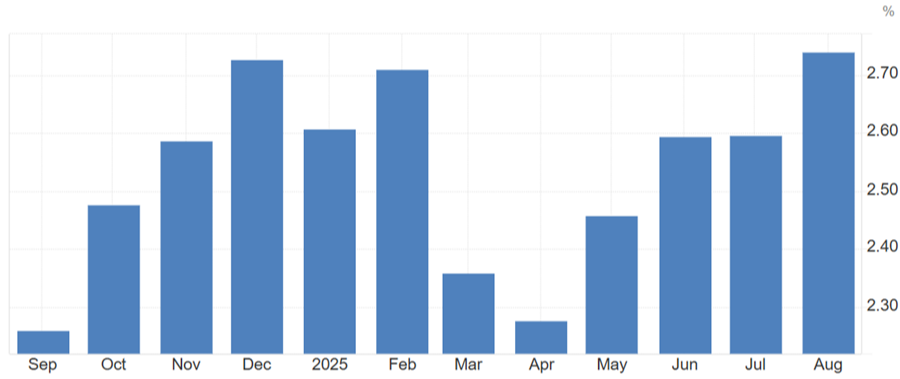

PCE Price Index - August +2.7% (YoY)

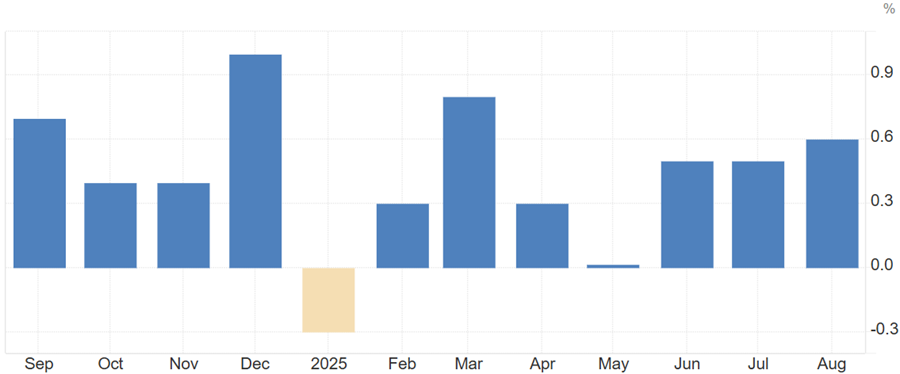

U.S. Personal Spending - August +0.6% (MoM)

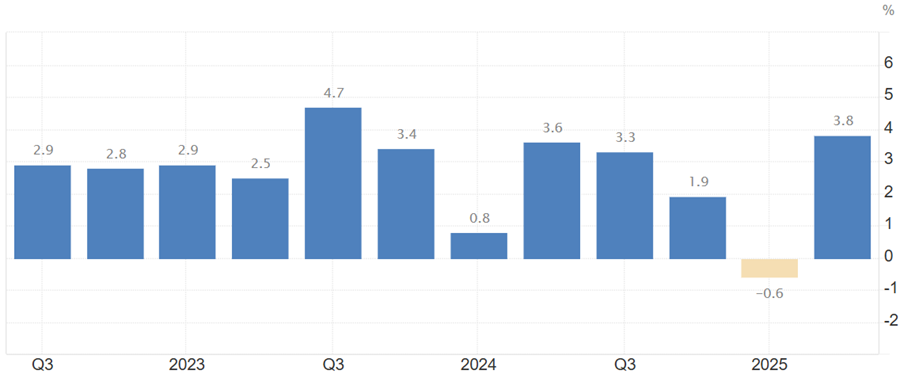

2Q25 GDP Growth Rate +3.8% (QoQ)

Earnings

Hyper-retailer, Costco Wholesale (COST), reported fiscal 4Q25 earnings and revenue above expectations. The company’s business model allows for flexibility and enhanced cost controls that have allowed Costco to continuously navigate tariff and inflation driven uncertainty.

Its membership model is a key component towards growth and was a highlight this quarter with fee income jumping 14% to $1.72 billion, driven by last year’s fee increase along with upgrades to the Executive memberships. The company is always looking to add unique value propositions, and the recent introduction of Executive-only shopping hours has already shown a 1% addition to weekly U.S. sales. Shopping categories demonstrated strength across the board with further strength from its Kirkland Signature brand aiding margin growth.

Given the company’s consistent outperformance, investors hold each earnings report to a high standard. The one blemish this time around was comparable sales growth of 5.7% falling shy of expectations – mainly due to gas price deflation and FX noise. Investors were more concerned from a competitive perspective with the recent development of Amazon (AMZN) beginning same-day grocery service, which could pressure Costco’s digital delivery efforts.

Despite this, COST posted another strong earnings release with a muted investor reaction, creating a reasonable buying opportunity as one of our core holdings.

Week Ahead

This week, focus will be on the labor market with the Job Openings (JOLTS) report to be released on Tuesday followed by the Employment report for September on Friday. Manufacturing and services PMI will print on Wednesday and Friday, respectively, as investors look to gauge economic growth trends.

On the earnings front, human capital management company, Paychex (PAYX), will be reporting its fiscal 1Q26 earnings before the market opens on Tuesday.

As always, if you have any questions or comments please do not hesitate to reach out.

Michael Neill, CFA

Chart Sources: TradingEconomics (US Census Bureau)