Market Summary – V is for Recovery

In early April, the tariff-induced uncertainty that weighed on sentiment throughout the first half of the year culminated in a correction for the S&P 500 and a bear market for the Nasdaq. At the time, it would have been difficult (impossible) to predict that in less than 12 weeks, the market would not only fully recover but also surpass its all-time high. As impressive as the market’s recovery has been, it does not seem like a complete surprise.

The volatility seen since late February has been primarily policy driven with uncertainty and fear of the potential impacts from tariffs slowing the economy and reigniting inflationary pressures. With the market at a premium valuation, participants were quick to sell first and ask questions later, fueling overwhelmingly negative sentiment and downside momentum.

The market began to rebound as these fears faded, despite continued back-and-forth policy uncertainty. Inflation continued to decline. The labor market remained resilient along with consumer demand. Earnings have been positive, driven by market-leading mega caps and semiconductors. Rate cut hopes remain high, despite Fed Chair Powell’s wait-and-see approach. Tariff escalations between the U.S and China have scaled back. And geopolitical tensions have calmed following the announcement of a ceasefire between Israel and Iran.

As we begin to step into the third quarter, the market has all these developments in mind and is consistently (frustratingly) looking forward. Following new record highs and rich valuations, the market has sufficiently priced in this optimism that may again lead to further bouts of volatility if those positive outcomes fall short of materializing as expected.

Still, as long-term investors, we remain focused on our plans and the fundamentals of the companies we own; instead of allowing our emotions to be dictated by changing sentiment, assumptions, or trends. Our goal is to use pullbacks as buying opportunities and avoid deviating from our plans and prematurely exiting the market. Below is a summary for the week and a brief outlook for the second half of the year.

The Week in Focus

Record highs followed the market’s reaction to a ceasefire between Israel and Iran, positive earnings from major companies, strong economic data, and dovish commentary from Fed Chair Powell in his testimony to Congress.

The ceasefire provided a sigh of relief for the market as oil prices fell and equities rallied, led by mega-caps and the growth-oriented sectors they tend to be in – technology, communications, and consumer discretionary.

The market lynchpin, Nvidia (NVDA), reached new all-time highs along with the broader market as it is now the largest company in the S&P 500 by market capitalization. The strong price action from Nvidia and related semiconductor names was driven by positive earnings from Micron Technologies (MU). Micron surpassed earnings and revenue expectations and, more broadly, reconfirmed the demand for further expansion of AI-infrastructure. Retail and discretionary sectors were also positively influenced by a welcomed strong earnings report from Nike (NKE).

Fed Chair Powell’s testimony to both the Senate and House spurred further optimism as Powell mentioned the possibility for inflation to be cooler than expected – contrasting the Summary of Economic Projections that the Fed released just last week indicating for the likelihood of elevated inflation given tariff uncertainty. The takeaway is that while not even the Fed is capable of accurately forecasting the future, rates are on the downswing with optimism that the Fed may increase the pace of rate cuts if inflation remains tamed.

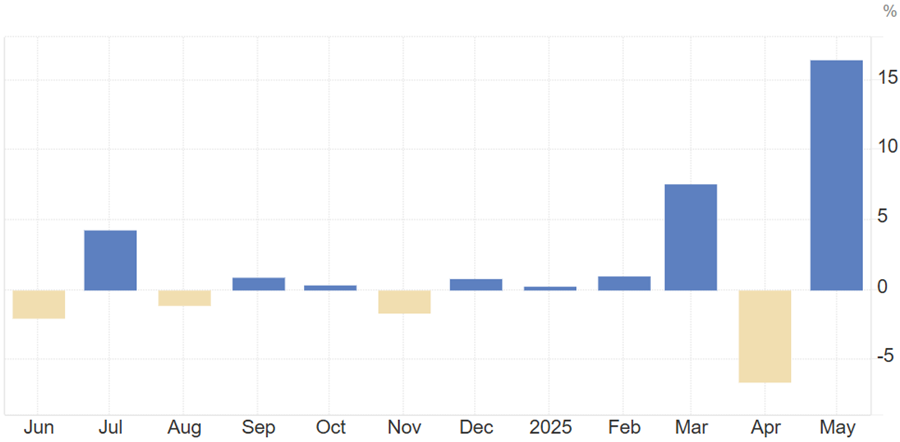

On the economic front, new orders for manufactured goods (durable goods orders) increased 16.4% in May, the largest jump since 2014, above expectations of 8.5%. The takeaway is that industrial demand rebounded following the pause of reciprocal tariffs. Importantly, new orders for non-defense goods excluding aircraft (a close proxy for general business activity) grew 1.7% in May from 1.4% in April.

Durable Goods Orders – May (16.4%)

Third Quarter Considerations

Despite the seemingly chaotic first half of the year, the market ended the second quarter on a high note. Going forward, scrutiny will continue to be placed on reciprocal tariffs as the pause on them expires on July 9th. In true Trump fashion, the possibility of another extension will likely be a last-minute decision and country dependent.

Also on the political front, the market will be watching developments related to the One Big, Beautiful Bill – President Trump’s proposed budget reconciliation bill. Key components of the bill will focus on extending the Tax Cuts and Jobs Act of 2017 and changes to Medicaid requirements and cost reductions. The takeaway from this is that deregulation and lower taxes are seen as positive for equity markets, but those benefits will likely clash with the uncertainty caused by further increases in the government deficit.

Market-specific drivers will center around 2nd quarter earnings, which will be one of the first litmus tests for valuations and the sustainability of the recent rally. Market participants will keep an eye on company guidance and commentary related to potential impacts from tariffs that will help gauge sentiment, as well. In the same thought, inflation data will be top of mind with the anticipation of two rate cuts by the Fed before year-end.

Week Ahead

This week, the Employment report for June will be released on Thursday as the market looks to gauge the continued resilience of the labor market. Key data in the form of the Manufacturing and Services Purchasing Managers Index (PMI) will help signal the strength of economic activity against the backdrop of tariff uncertainty and reduced spending. Second quarter earnings will begin with major banks on July 15th.

As always, if you have any questions or comments please do not hesitate to reach out.

Chart Sources: TradingEconomics