Market Summary

Major equity indices continued last week’s theme of hesitancy, but ended little changed as new uncertainties emerge surrounding the Israel-Iran war and, more specifically, the extent of the United States’ involvement.

Geopolitical tension overshadowed the Federal Reserve’s decision to maintain rates unchanged, with Fed Chair Powell continuing to pursue a wait-and-see approach, given upside risks to inflation spurred by tariffs.

The nod to the possibility of higher inflation left the treasury market unphased, with yields dropping primarily due to a flight of safety by investors due to geopolitical angst.

Investors also had the chance to parse through some housing data, which pointed towards a continued contraction due to higher rates with a slowing of permits and housing starts. Retail Sales for May declined -0.9% from the previous months largely due to consumers pulling back spending in the face of tariff uncertainty.

Israel-Iran Conflict

The market saw another bout of back-and-forth action as rhetoric over the Israel-Iran conflict spanned from negotiation and patience to demanding Iran’s unconditional surrender. This turned quickly to a direct attack by the U.S. on key nuclear facilities in Iran, implying the decision had already been made for some time.

So far, the market has largely been unphased with sentiment dismissing the prospect of any possible retaliation by Iran disrupting oil supplies. Regional tensions continue, but there has not yet been further escalation.

This, of course, could all change but the takeaway is that while the events are unnerving, the involvement of the U.S. has not translated into any negative economic impact. The consideration going forward will be the extent of future U.S. military action, which will largely stem from the extent of Iran’s retaliatory measures.

The Fed

On Wednesday, the Fed behaved as expected, voting unanimously to maintain the fed funds range unchanged at 4.25-4.50%. Despite many market participants (and politicians) believing the Fed has the green light to cut rates, Fed Chair Powell cited upside risks to inflation given tariff uncertainty. Powell articulated the need for more time to assess future data with the expectation of elevated inflation in coming months. The market was a bit agitated and treasury yields briefly rose, but the overall reaction was relatively muted.

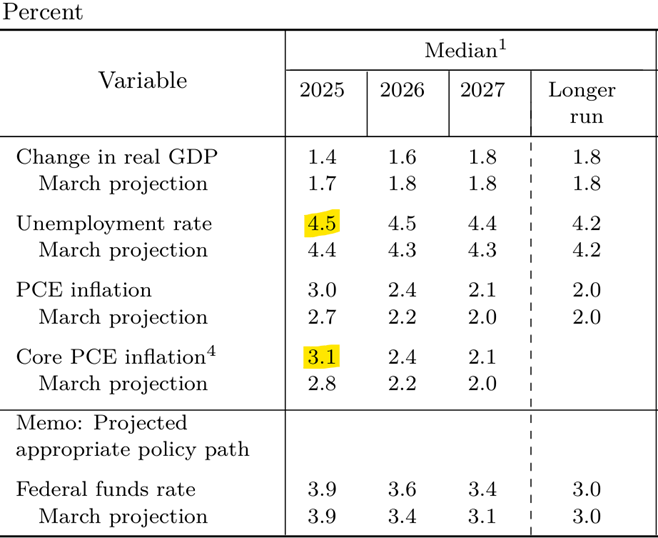

The FOMC meeting was accompanied by an updated Summary of Economic Projections (SEP), which gave conflicting information in terms of maintaining the expectation of two rate cuts before year-end but depicting an increase in inflation expectations. Unemployment expectations were also raised. Fortunately, or unfortunately, the Fed has a horrible track record of forecasting these things – excerpt below for your interest.

Table1. Economic Projections of Federal Reserve Members (June 2025)

Asset Allocation & Performance

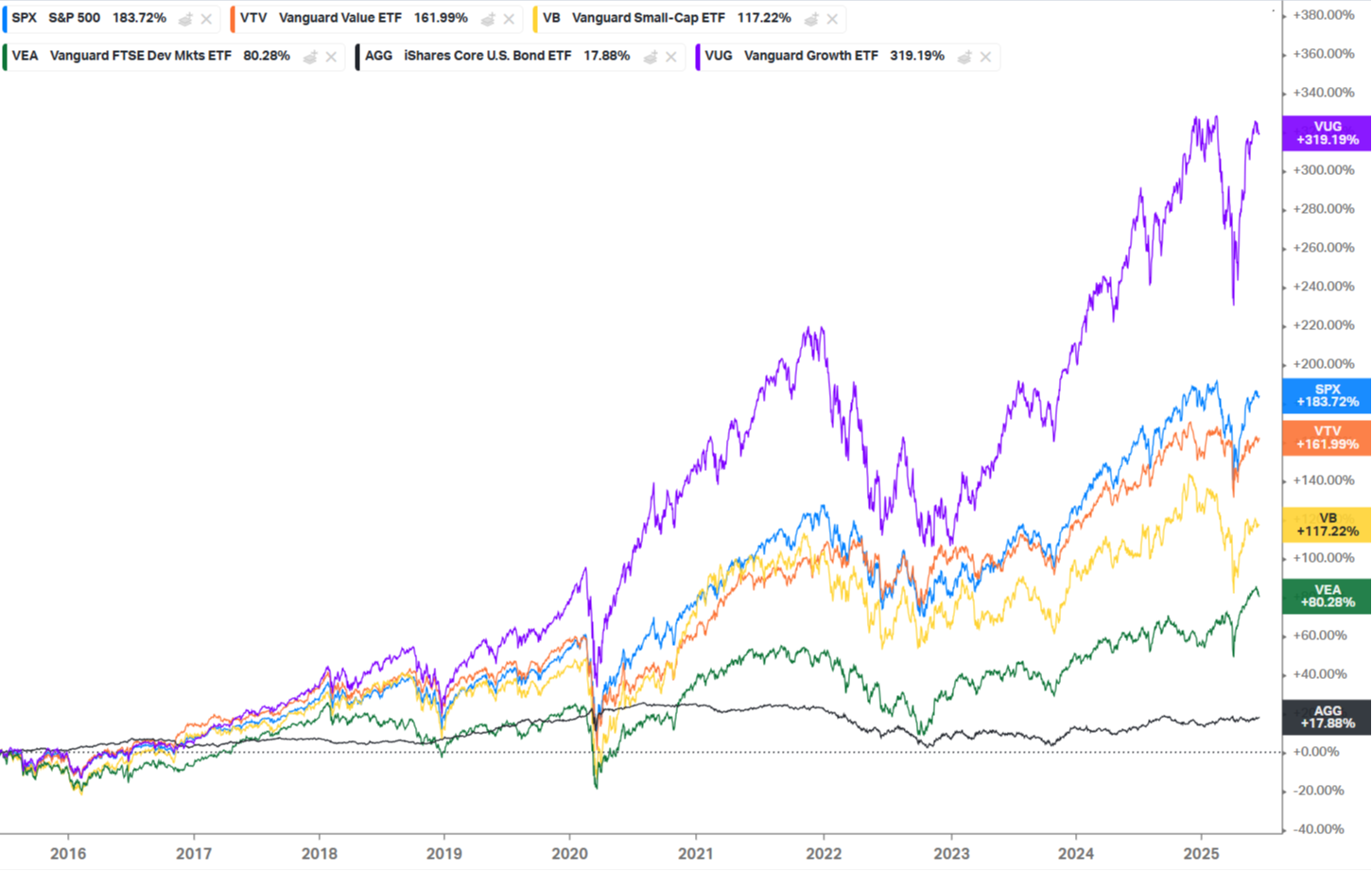

Below is a chart depicting the performance of major asset classes over the last 10 years. A brief description of each follows.

S&P 500 – The blue represents the largest 500 U.S. companies and what people generally refer to as ‘the market.’ The S&P 500 consists of a mix of both growth and value stocks and is a good representation of all major sectors of the economy. Performance wise, the S&P 500 tends to sit somewhere between the growth and value ends of the spectrum.

U.S. Large Cap Growth – well establish companies that prioritize growing earnings and revenue faster than the overall market. These companies tend to reinvest profits, rather than paying a larger dividend, to fuel expansion. Common sectors are information technology, consumer discretionary, and communications. Investors are willing to pay a premium for the prospect of greater future cash flows, which can lead to these stocks experiencing greater bouts of volatility compared to the broader market.

U.S. Large Cap Value – traditionally lower volatility companies that prioritize stable cash flows and dividends. They tend to be undervalued relative to their own fundamentals and are commonly found within non-cyclical sectors, such as financials, industrials, consumer staples, and utilities.

U.S. Small Cap– yellow represents smaller U.S. companies that tend to have higher growth potential relative to their large cap counterparts.

Developed International – Green depicts a broad benchmark for companies in developed markets outside of the U.S., including Europe, Canada, Japan, and Australia. For simplicity, we excluded emerging markets like China and India. Both asset classes have historically underperformed the S&P 500 over the last 20 years.

Aggregate Bond Index – the last item on the chart is the aggregate bond index, a broad benchmark for the investment-grade bond market in the U.S.

A few takeaways:

Patient and disciplined investors find success over time. Staying invested and not allowing our emotions to dictate our investments are key – but so is investing in the right areas of the market.

The U.S. stock market has been the place to be. It has outperformed every other asset class like cash, bonds, international markets, commodities, and real estate. It has also outperformed gold over the long term.

Cash and fixed income allocations tend to lower volatility and are important considerations for those who need it, but they have proven to be a significant drag on performance. Overly conservative allocations can have a negative impact on the potential for retirement portfolios if done too early.

Our portfolios prioritize investing within the growth-oriented areas of the U.S. market with diversification towards core, value, small-cap, and international companies.

While frequent periods of uncertainty may prompt the market to waver (especially the growthier end of the spectrum), the market has consistently shown its ability to very quickly and strongly bounce back.

Time is our friend. In times like this, it is important to widen our view and keep things in perspective.

Week Ahead

This week, market participants will continue to digest the Israel-Iran situation and look towards sparse economic data, including inflation for May in the form of Core PCE on Friday. On Tuesday and Wednesday, Fed Chair Powell will deliver his semi-annual testimony to Congress. The expectation is for the Republican side of the aisle to vilify Powell for electing to not cut rates last week.

As always, if you have any questions or comments please do not hesitate to reach out.

Chart Sources:

Federal Reserve Board

MFG, Koyfin