Market Summary

The S&P 500 ended the week relatively flat as the start of the week was marked by optimism for high-level trade talks in London, which later produced a muted market response as little progress was made between the U.S. and China outside of what was originally agreed upon in prior talks.

This news ultimately overshadowed pleasing inflation data for May. While the market demonstrated resilience throughout the week, Friday brought heightened pressure as Israel struck nuclear facilities and military installations in Iran overnight – which led to retaliatory missile strikes by Iran over the weekend.

Oil prices spiked in response, sparking some volatility and throwing another wrench in the inflation picture ahead of the upcoming Fed meeting on June 18. While the U.S economy is significantly less reliant on imported oil than in the past, comparisons can be drawn to the dynamics around the 1979 Iranian Revolution, elevated energy prices, and the potential for a resurgence in inflation – all of which will be in the back of the mind of Fed Chair Powell this week.

Inflation – CPI and PPI

The key piece of market moving economic data for the week were inflation readings for May – which continued to show a declining trend, inviting anticipation for rate cuts.

On a yearly basis, headline inflation increased 2.4% in May from 2.3% in April; while core inflation, excluding food and energy, remained unchanged at 2.8% in May.

If you were to also exclude housing costs, super-core inflation increased just 1.8% on a yearly basis.

The takeaway is that May marked the fourth month that inflation has maintained lower, stable levels that many consider to be within the Fed’s target range. At this point, all eyes are on the Fed to see if recent data are enough to justify a rate cut – data which now reflects some tariff activity such as the 10% baseline tariffs and 25% tariffs on aluminum, steel and autos.

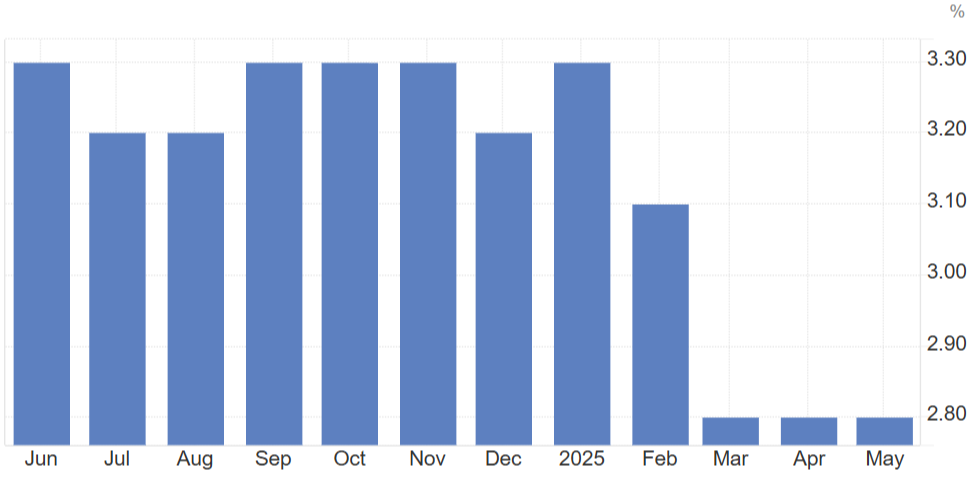

U.S. Core Inflation – May (2.8%)

Week Ahead

This week, market participants will be focused on the Fed’s next interest rate decision on June 18 just before the Juneteenth holiday. Importantly, this Fed meeting will offer additional commentary from Fed Chair Powell with an updated Summary of Economic Projections. The market will also have an eye on the Bank of Japan and its interest rate decision on Tuesday. Retail Sales for May will release early on Tuesday along with housing data throughout the week.

As always, if you have any questions or comments please do not hesitate to reach out.

Chart Sources: MFG, TradingEconomics